Infrastructure Half-Life

Infrastructure Half-Life is the period over which a physical asset retains its economic relevance. It is not the same as engineering life. A gas engine can run for 25 years. A transformer can run for 40. Whether anyone will pay for what they produce in year 12 is a separate question, and it is the question that matters.

For most of the last century the two lives moved together. Power plants, substations, and transmission lines were built against demand that changed slowly. An asset wore out at roughly the same rate it became obsolete. Underwriting could treat engineering life as a reasonable proxy for economic life, and it did.

AI data center power infrastructure has broken that relationship. The technology it serves now turns over faster than the assets themselves. Compute generations last two to three years. Rack densities have moved from 10 kW to over 130 kW in five years. Cooling architectures are being replaced mid-deployment. The power infrastructure procured against these loads was financed on 15 to 25 year assumptions.

The result is a structural gap. The economic half-life of AI power infrastructure is materially shorter than its engineering life, and most of the capital entering the sector is priced as if the two were still the same.

Why the half-life is compressing

Four forces are shortening the period over which these assets hold their value.

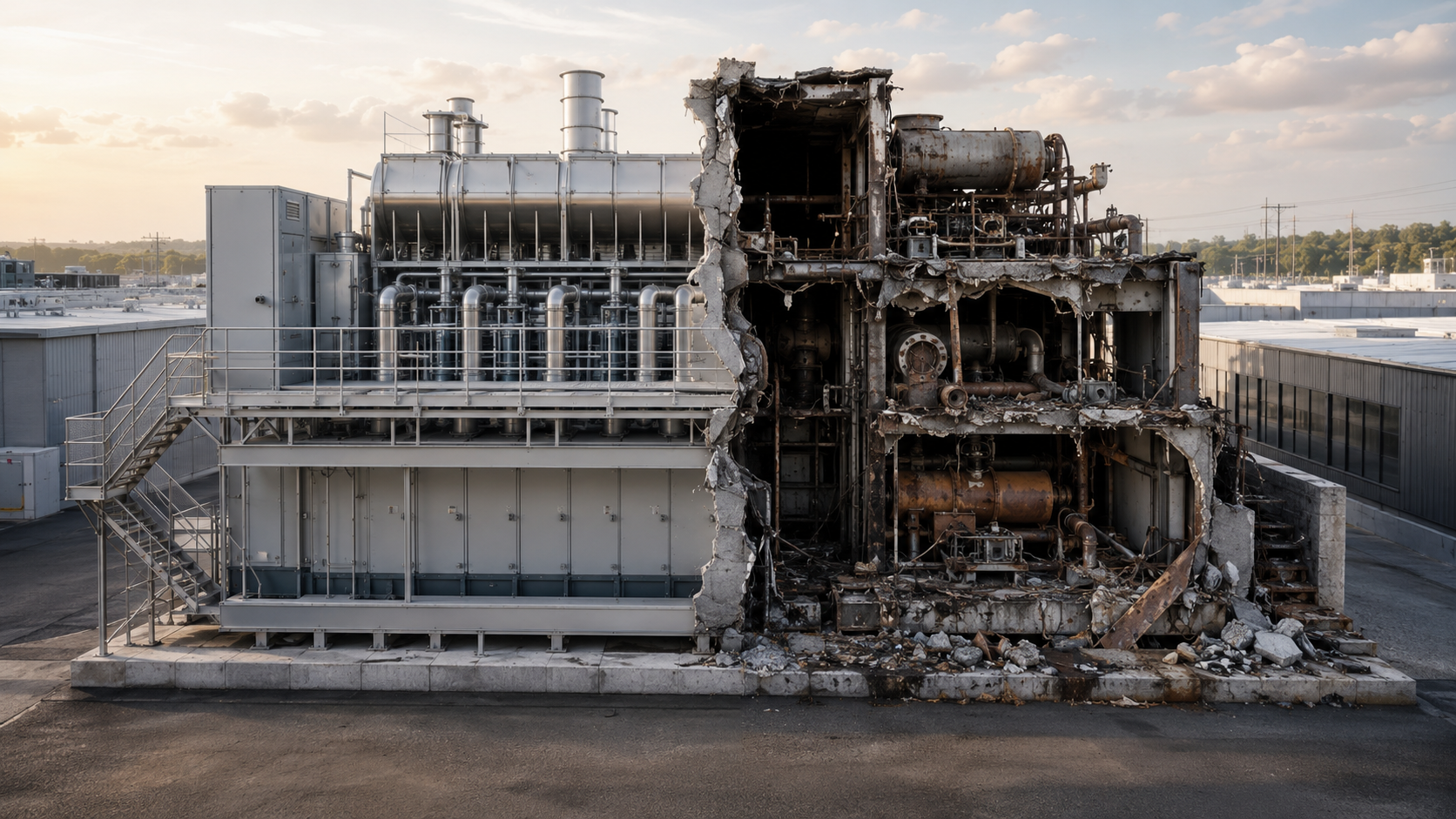

The first is technology turnover. Power and cooling infrastructure is specified against the compute it serves. When the compute changes, the specification ages. A facility engineered for air-cooled 15 kW racks does not gracefully absorb 130 kW liquid-cooled deployments. The building stands. Its economic purpose does not.

The second is counterparty concentration. A large share of contracted AI load sits with a small number of tenants whose own revenue models are unproven at scale. An engine hall with a 20 year design life and a 7 year tenant commitment has an economic life defined by the tenant, not the engine. The industry has been slow to price the difference.

The third is the bridge power wave. Thousands of megawatts of reciprocating engines and gas turbines have been deployed as interim solutions while grid interconnection catches up. These assets were procured for speed. Almost none were procured with a defined second act. When the grid arrives, or the load moves, or the market corrects, this fleet needs an answer: redeploy, repower, resell, or write off.

The fourth is regulatory drift. Cost allocation rules, large-load tariffs, and ratepayer protection frameworks are being rewritten in real time. An asset that pencils under today's tariff structure may not pencil under the one enacted three years from now. Political half-life is now a component of economic half-life.

The underwriting error

Here is the practical failure. Infrastructure capital prices two things well: construction risk and operating risk. It prices a third thing badly: relevance risk. The risk that an asset, fully built and perfectly functional, stops being the thing the market wants.

You can see the error in how residual value is treated. Most models carry residual value as a terminal assumption, a single number in the final year, lightly stressed. For long-lived grid assets that was defensible. For AI power infrastructure, residual value is not a terminal detail. It is a primary driver of returns, because the probability that the asset outlives its first use case is high and rising.

The correction is to underwrite survivability, not just speed. That means asking a different set of questions at acquisition. Can this asset serve a second load if the first one leaves? What does redeployment cost, physically and contractually? Is the technology modular enough to move, or is it stranded by its own foundations? Does a secondary market exist for it, and at what discount?

The redeployment hierarchy

Not all assets age the same way, and this is where the half-life framework becomes an investment tool rather than an observation.

Reciprocating gas engines sit near the top of the hierarchy. They are modular, containerized or skid-mounted, fuel-flexible, and supported by a mature global secondary market with established refurbishment channels. An engine that finishes its bridge duty at a data center can move to industrial CHP, grid peaking, biogas, or microgrid service. Its economic life can be extended through relocation in a way a purpose-built facility's cannot.

Gas turbines are more constrained. They redeploy, but at higher cost, with heavier balance-of-plant, and into a narrower set of second uses. Batteries occupy a middle position: chemically aging assets with genuine locational flexibility. At the bottom sit the site-specific assets: substations, dedicated transmission spurs, liquid cooling plants, and the buildings themselves. Their engineering life is the longest in the stack and their redeployment optionality is the lowest. That combination, long life plus low optionality, is precisely where relevance risk concentrates.

The hierarchy inverts some current pricing. The market pays a premium for permanence. The half-life framework says permanence without optionality is a liability, and that mobility, fuel flexibility, and secondary market depth deserve a premium they are not currently receiving.

The demand floor

The half-life argument would be incomplete, and considerably more pessimistic, without one countervailing fact. While AI load may overbuild, the underlying trend in commercial and industrial demand runs the other way. C&I electricity consumption is rising, and peak demand is rising faster than average demand. Electrified heat, EV fleets, industrial electrification, and reshored manufacturing are all peak-heavy loads landing on a grid that cannot expand at the pace they arrive.

This matters because it gives displaced AI power assets a natural second home. A rising-peak world is a world that needs exactly what the bridge fleet provides: dispatchable, distributed, behind-the-meter capacity that can shave peaks, firm supply, and anchor microgrids. If the AI buildout overshoots, the surplus does not fall into a vacuum. It falls into a market with growing structural demand for flexible megawatts.

But the demand floor is conditional, and the condition is the whole point. C&I buyers do not pay panic prices. They will absorb redeployed assets only if redeployment is cost and time competitive with new build. An engine that can be demobilized, moved, recommissioned, and contracted faster and cheaper than a new unit finds a buyer. An asset whose relocation cost approaches replacement cost does not, whatever the demand backdrop. The demand floor exists, but each asset must reach it, and the ability to reach it is exactly what the redeployment hierarchy measures.

This changes the shape of the risk. For high-optionality assets, the AI correction scenario is not a write-off scenario. It is a discount-and-redeploy scenario, with the discount set by mobilization cost and speed rather than by absence of demand. For low-optionality assets, the demand floor offers no rescue, because they cannot travel to where the demand is. The gap between the top and bottom of the hierarchy widens rather than narrows in a downturn.

Measuring it

A framework that cannot be measured is a slogan. Infrastructure Half-Life can be estimated for any asset class by combining four observable inputs: the turnover rate of the technology the asset serves, the tenor and credit of the contracts behind it, the depth and discount of its secondary market, and the cost of its conversion to a second use as a share of replacement cost.

An asset serving fast-turning technology, backed by short contracts, with no secondary market and high conversion costs has a short half-life regardless of its nameplate design life. An asset with the opposite profile can have an economic life that exceeds its engineering life, because redeployment resets the clock.

I will publish estimates for the major asset classes in AI power infrastructure, and I will keep them on the record. Two claims are worth timestamping now (July 6th 2026). First, by 2029 a visible secondary market in data center bridge power assets will exist, with published pricing, because the current deployment wave guarantees the supply. Second, residual value and redeployment assumptions will migrate from terminal-year footnotes into headline underwriting criteria for data center power transactions before the end of the decade. If neither happens, the framework failed. I do not expect it to fail.

Where this sits

This framework extends an argument I have been making for several years. The Temporal Trilemma described the timing problem: speed, cost, and permanence cannot all be optimized at once. The Structured Transition Model described how infrastructure should evolve through staged configurations rather than single end-state bets. Speed to Power described the sprint phase the industry is in now, where time to energization outranks almost everything.

Infrastructure Half-Life describes what comes after the sprint. The industry sorted first on speed. It will sort next on durability, and durability will belong to the assets and contracts that were underwritten to survive their first use case, not just to reach it. The capital that understands this early will buy optionality cheaply. The capital that does not will discover, at the first correction, that it financed 25 year assets against 7 year certainty.

The engine keeps running, and somewhere a factory, a hospital, or a fleet depot needs its output. The question is whether the engine can get there at a cost and speed the buyer will pay. That question, asked at acquisition rather than at distress, is the whole framework.

Read More

Five Nines and Fast Power

Making Better Energy Decisions in Data Center Investments

-

Infrastructure Half-Life is the period over which a physical asset retains its economic relevance. It is distinct from engineering life, which measures how long the asset can physically operate. For AI data center power infrastructure, economic half-life is now materially shorter than engineering life.

-

Engineering life is set by physical wear and maintenance. Economic life is set by whether the market still pays for what the asset produces. A gas engine can run for 25 years, but if its load disappears in year 7, its economic life ended in year 7 unless it can redeploy.

-

Four forces compress it: compute technology turns over every two to three years while power assets are financed over 15 to 25, contracted load is concentrated in a small number of tenants with unproven revenue models, thousands of megawatts of bridge power were deployed with no defined second act, and tariff and cost-allocation rules are being rewritten in real time.

-

It means underwriting survivability, not just speed. Residual value and redeployment cost should move from terminal-year footnotes to headline acquisition criteria. The key questions are whether an asset can serve a second load, what relocation costs, and whether a secondary market exists for it.

-

Modular, mobile, fuel-flexible assets with deep secondary markets. Reciprocating gas engines rank highest because they can move from data center bridge duty to industrial CHP, grid peaking, biogas, or microgrid service. Site-specific assets such as substations, dedicated transmission spurs, and purpose-built facilities rank lowest because they cannot travel to new demand.

-

For mobile assets, a correction is a discount-and-redeploy event, not a write-off. Commercial and industrial peak demand is rising and needs dispatchable, distributed capacity. But that demand floor only rescues assets that can redeploy at a cost and speed competitive with new build.

-

By combining four observable inputs: the turnover rate of the technology the asset serves, the tenor and credit quality of the contracts behind it, the depth and discount of its secondary market, and conversion cost to a second use as a share of replacement cost.

-

Speed to Power describes the current sprint phase, where time to energization outranks almost everything. Infrastructure Half-Life describes what comes after: the market will sort next on durability, and the assets underwritten to survive their first use case will hold their value.