The AI Bubble May Burst. The Power Deficit Remains.

Even if AI investment slows, most of the power demand does not.

The question being asked about AI is whether the spending is justified. The five largest US cloud and AI companies are guiding toward $635 to $690 billion in combined capital spending in 2026, more than double the 2024 level, with roughly three quarters of it going to AI infrastructure. Skeptics point to the economics. Microsoft disclosed in January 2026 that $37.5 billion of a single quarter's spending went to short-lived assets, mainly graphics processing units (GPUs) and central processing units (CPUs) with useful lives of three to five years. Whether that spending makes sense is a fair debate.

My question is different. If AI investment corrects, what happens to power demand?

The answer is that it holds. Most of it was never AI.

Back in 2017, the discussion was only around a resilient grid providing power to data centers with diesel engines providing back up energy. The move to onsite power has been rapid over the last 1-2 years. Now, the point that follows from it is rarely stated directly: if AI spending slows, power generation is more resilient than the AI narrative implies, because the demand underneath it does not depend on AI.

The assumption I will grant

Assume the skeptics are right. Assume a meaningful share of AI capital spending does not earn its return and the cycle corrects, as capital cycles tend to. The relevant question for anyone who builds or finances power generation is not whether that happens. It is how much demand survives it.

Most of the demand is not AI

Start with the load itself. The IEA's Electricity 2026 report finds that US electricity demand grew 2.1% in 2025 and is projected to grow close to 2% a year through 2030, with around half of that increase driven by data centers. Half is the share attributable to AI and the rest of the data center buildout. The other half is not.

That other half is not speculative. Deloitte's 2026 power and utilities outlook projects US peak demand rising about 26% by 2035 and expects industrial electrification alone to add around 25 GW by 2030, on top of growth in household and commercial use. Rabobank estimates the system peak rising from about 760 GW today to between 850 and 930 GW by 2030, driven by data centers, electrified transport, and industrial reshoring together. The EIA describes this as the reversal of nearly two decades of flat demand, with the growth split between the commercial sector, which includes data centers, and the industrial sector, which includes manufacturing.

Electrification, reshoring (of manufacturing to the US), and grid balancing for a changing generation mix do not run on AI capital cycles. They continue whether or not the next training cluster gets built. An AI correction removes part of one half of the growth. It leaves the rest in place.

Supply cannot meet even that floor

The resilience is reinforced from the supply side. New data center projects already face delays of 24 to 72 months because of shortages of transformers, switchgear, and generating assets. Utilities are spending to catch up, with capital spending up about 20% in 2025 and a forecast 15% in 2026, and that spending still lags demand.

The supply chain cannot satisfy the non-AI demand on its own. In that setting, an AI correction does not produce surplus capacity. It relieves pressure on a system that is already short. The equipment, the interconnection capacity, and the generation are constrained before AI is added, not after.

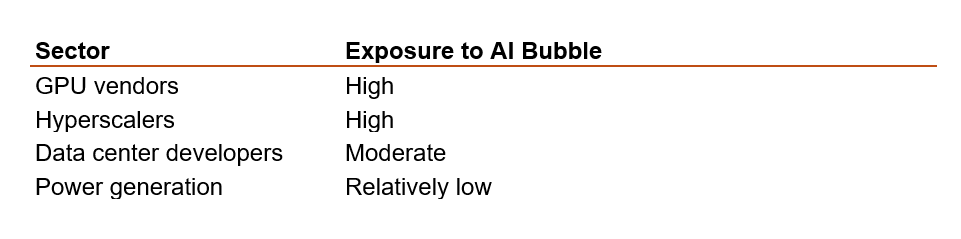

Comparison of different organizations exposure to AI bubble

Two objections

The first is that interconnection queues are inflated by speculative AI projects, so a bust deflates them. That is partly true, and it is the reason the durable signal is the demand floor, not the queue. The floor does not depend on speculative projects clearing. The electrification and industrial load is already arriving.

The second is that the dot-com bust left a glut of fiber, so an AI bust could leave a glut of power. The assets are not comparable. Fiber was a single-purpose asset that became cheap when one source of demand fell away. Power serves many loads at once, and it is physically supply-constrained. When one source of demand softens, the capacity is absorbed by the others rather than stranded. A demand reduction in a short market relieves scarcity. It does not create a surplus.

Much of the excess fibre installed during the dot-com era was eventually absorbed as internet adoption expanded. The difference is that electricity infrastructure begins from a position of shortage rather than excess. Even if AI demand moderates, capacity is likely to be absorbed more rapidly because the broader economy is already electrifying.

What this means for power generation

Power generation companies are not levered to AI the way the hyperscalers are. Their demand base is broad: electrification, manufacturing, grid balancing, resilience, and the replacement of an aging fleet. An AI correction would slow one customer segment. It would not slow the market.

The exposure sits with the constraint, not the valuation cycle. Flexible and dispatchable generation, microgrids, combined heat and power, storage, and speed-to-power solutions are demanded because the system is short of capacity and short of the equipment to add it. That shortage exists independently of what happens to AI spending. The work I have framed through the Structured Transition Model is about sequencing investment under exactly this kind of constraint, where the binding limits are speed, resilience, and economics rather than the direction of a single demand source.

The point

The AI bubble may or may not burst. Either outcome leaves the same picture. Power demand rests on a base that is mostly not AI, against a supply chain that cannot keep pace with that base on its own. Power generation is resilient to an AI correction because the demand was never mostly AI in the first place.

More Reading

Structured Transition Model for AI Data Center Power

Questions and answers

Will power demand collapse if the AI bubble bursts?

No. Most of the growth in US electricity demand does not come from AI. The IEA's Electricity 2026 report attributes only around half of projected US demand growth through 2030 to data centers. The rest comes from electrification, manufacturing, and grid balancing, none of which depend on AI capital cycles. A correction in AI spending would slow one part of the growth and leave the rest in place.

How much of US electricity demand growth comes from data centers?

Around half. The IEA reports that US electricity demand grew 2.1% in 2025 and is projected to grow close to 2% a year through 2030, with roughly half of that increase driven by data centers. The other half is driven by electrified transport, industrial reshoring, and the broader electrification of buildings and industry.

If AI spending slows, what happens to power generation companies?

They are far less exposed than the hyperscalers. Power generation companies serve a broad demand base: electrification, manufacturing, grid balancing, resilience, and the replacement of an aging fleet. AI is one customer segment within that base, not the market itself. An AI correction would slow that segment without removing the underlying demand.

Could an AI bust create a power capacity glut, like the dot-com fiber glut?

It is unlikely, because power and fiber are not comparable assets. Fiber was a single-purpose asset that became cheap when one source of demand fell away. Power serves many loads at once and is physically supply-constrained. If one source of demand softens, the capacity is absorbed by the others rather than stranded. In a market that is already short of capacity, a reduction in demand relieves scarcity rather than creating a surplus.

Are interconnection queues inflated by speculative AI projects?

In part, yes. Many queued projects are speculative and will not be built, so the queue overstates firm demand. This is why the durable signal is the underlying demand floor from electrification and industry, not the queue. That floor is already arriving and does not depend on speculative projects clearing.

Is power or compute the binding constraint on AI infrastructure?

Power. The availability of electricity, generation capacity, and grid equipment now limits where and how fast AI infrastructure can be built. New data center projects face delays of 24 to 72 months because of shortages of transformers, switchgear, and gas turbines. I argued in 2017 that power, not compute, would be the constraint, a view that is now widely shared.

Why is power infrastructure demand considered resilient to an AI correction?

Because the demand rests on a base that is mostly not AI, against a supply chain that cannot keep pace with that base on its own. Even a significant reduction in AI investment leaves substantial demand from electrification, manufacturing, and grid balancing, in a system already short of capacity and the equipment to add it.